When it comes to insuring your business, the traditional market is already difficult to comb through. When considering captive insurers, there is so much variety to choose from for your business. You have group captives. You have cell captives. And, yes, you can go the single-parent captive route. The most difficult thing is determining which route to take to best insure your business.

But what exactly is a single-parent captive? How can they benefit your business? And what are their challenges?

ReNu Insurance Group has many years of experience answering these questions, especially when we’ve helped over 130 businesses become captive owners. It’s our responsibility to understand the ins and outs of single-parent captives. With our experience and expertise, we’ve learned that single-parent captives are great for some businesses and aren’t the ideal solution for others.

In this article, you’ll learn about what single-parent captive insurers are, what they can provide for your business, their benefits, their challenges, and how they’re different from group captives. After reading, you can determine if single-parent captives are right for your business or if you need to figure out an alternate solution for your insurance needs.

And take your captive assessment to see if your business is the right fit for captive insurance.

Table of Contents:

- What is a single-parent insurance company?

- What do single-parent captives provide for my business?

- How are single-parent and group captives different?

- Since my business would own the single-parent, am I now part of the insurance industry?

- So, is a single-parent captive right for your business?

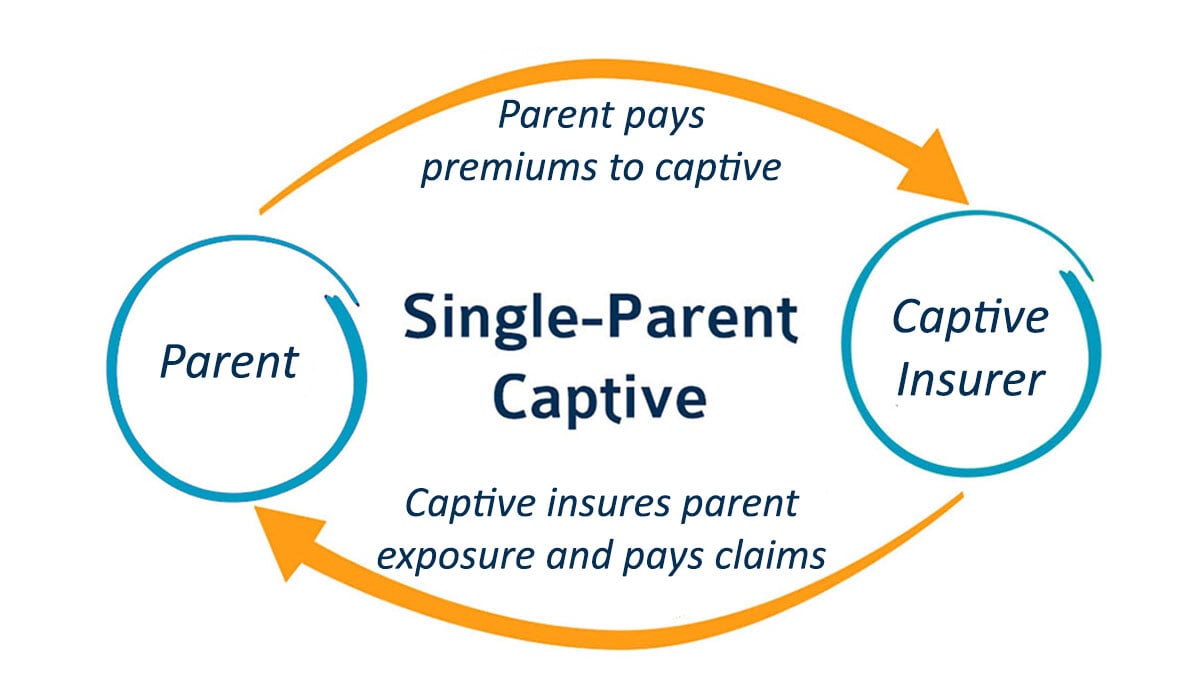

What is a single-parent captive insurance company?

A single-parent captive is an insurance company created to cover the risk of the parent (aka your business). These are otherwise known as a "Pure" captive. Your business owns the insurer. There isn’t a mixing of other businesses like there would be with a group captive.

To make a single-parent captive work, you need to have scale. Even though the single-parent captive is a subsidiary of the parent, it still needs to comply with IRS regulations as true notions of insurance. So you’re transferring the legitimate risk of fortuitous events. You need to have enough risk shifting and distribution so the IRS says, “Yep, this is real insurance.” The last thing you want is for the IRS to hate your captive.

This is a long-winded way of saying single-parent captives are legitimate.

If your single-parent captive needs a fronting carrier (most do), you will still need collateral. Your regulator will dictate how much money you need, and the IRS wants to ensure you have true insurance notions.

Note: the IRS mandates that these captives demonstrate sufficient risk distribution and risk shifting to qualify as legitimate insurance entities. This requirement often means that single-parent captives are used by businesses with significant scale and variety of risk exposures.

How common are single-parent captives?

Single-parent captives are very common! They’re a pretty prevalent choice in the captive insurance market. For perspective, two-thirds of all captives are single-parent.

To provide a sense of scale, single-parent captives are a favored structure for larger corporations looking to gain more control over their insurance expenditures and risk management strategies. As the decades have passed, single-parent captives have become more accessible to small—to mid-sized businesses.

What do single-parent captives provide for my business?

When you take on risk and put it into a captive, you get complete transparency and can see where every dollar is allocated. You have to know where every dollar goes and why it goes there. You really get to decide on how much risk you want to take.

Whether it’s a single-parent or group captive, there is a famous saying in the industry: if you’ve seen one captive, you’ve seen one captive. This is because each captive is set up unique to that particular business.

Every captive insurer is different since you can do virtually anything with them (assuming the regulator lets you). Particular domiciles won’t let you do certain things in a captive. So, you need to figure out where you want your captive insurer to live.

Benefits of single-parent captives

While every business is different, many of them have found similar benefits in switching to this type of captive insurance program.

- Control - Businesses have more autonomy over risk management and insurance programs that fit their specific needs.

- Flexibility - A single-parent captive, with regulator approval, offers the ability to add just about anything (so long as it meets IRS rules). You aren't restricted to only Workers’ Compensation, Auto, or General Liability. For example, you can add a property deductible to your policy.

- Cost Efficiency—Like with any captive insurer, businesses can potentially reduce insurance costs by retaining underwriting profit. Compare this to a traditional insurer, which pockets all the money.

- Enhanced Risk Management - Single-parent captives encourage and reward business owners for being proactive with risk management, especially when a direct financial stake is involved with their insurance entity.

Challenges with single-parent captives

While the benefits make single-parent captives look tempting, it would be a lie to say they’re suitable for everyone. Before moving forward, you need to seriously consider the challenges.

- Capital Requirements - Creating a single-parent captive requires substantial capital investment. Your business needs to finance the captive adequately to ensure its viability.

The industry recommends at least $1 million in premiums. Depending on your industry, what you are putting into the captive, and if you need a front, you could get away with a little more or less.

Remember: Captives are a long-term risk financing tool. You’re financing your risk with your own insurance carrier rather than paying a third party to take it on. - Regulatory oversight - Single-parent captives are subject to strict regulatory oversight. This includes compliance with domicile regulations and the IRS’s criteria for insurance entities.

A happy wife plus a happy IRS equals a happy life. Or, however, the expression goes. - Risk of significant losses - A group captive has money pooled with other entities in preparation for large losses. With a single-parent captive, you’re more or less on your own (sort of).

The business assumes the entire risk in a single-parent captive, so if large or multiple claims occur, the financial impact can be very severe. This is why effective risk management and adequate reinsurance are essential to mitigate this risk. You also determine what retention that captive is taking versus what it is laying off in the commercial market or fronting carrier.\

It’s important to understand how layering works in the insurance industry and where the attachment point of your captive is. It’s a cost-benefit analysis summarized, “Is the juice worth the squeeze?” - Operational responsibilities - Managing a captive requires administrative and operational duties, including regulatory filings, financial management, and claims processing. Most businesses hire a captive manager to handle these tasks to mitigate this challenge.

How are single-parent and group captives different?

To accomplish everything that would allow the IRS to be okay with your premiums being deductible for federal income tax, you have to do it internally on your own. Compare this to someone else doing it in a group captive.

In a group captive, whether heterogeneous or homogeneous, you share risk among unrelated entities. In a single-parent, all entities are subsidiaries of the parent.

For a better understanding of the differences between single-parent and group captives, watch this video:

Do I have more control over premiums and rates in a single-parent captive?

An actuary – business professionals who mathematically analyze the financial consequences of risk and uncertainty – needs to sign off on your feasibility study to begin. They give the five-year feasibility study answer to the regulator, “Is this thing going to live long enough to pay claims?”

Sure, you own the insurance company. Either way, the single-parent captive needs to have the finances to pay claims and be actuarially sound.

As for what you can put in the captive, you get more flexibility since you own the whole thing. You don’t need to ask permission (though your domicile regulator will have a say in what you can and cannot add). So if you want to put cyber insurance in your single parent, you can–assuming it’s legitimate insurance for your business, and you check all the boxes with the IRS.

Compare this to a group captive. If one weren’t set up to offer cyber, you couldn’t add that to your policy.

Since my business would own the single-parent, am I now part of the insurance industry?

This is a surprisingly common question. No, owning a single-parent captive doesn’t mean you’re suddenly competing with other insurance companies. You just own the captive. The captive manager takes care of everything going on in the single-parent.

Typically, the risk managers are the ones selecting the vendors and owners. They’re the ones managing the organization and risk of the single parent. So you can run your business as usual while captive managers and risk managers take care of everything in the single-parent setting.

So, is a single-parent captive right for your business?

When it comes to gaining control over your insurance and risk management profiles, single-parent captives are a powerful tool. However, they require careful planning, investment, and commitment to ongoing risk management.

As you continue looking for optimal insurance solutions for your business, you’ll want to read our article on the pros and cons of single-parent and group captives. See which solution might be the better fit for you.

If you're wondering how much you would need to be a captive owner and how much your business can make in underwriting profit, take our pricing calculator to see your results.

{kind=link}