You’ve taken the hit of paying higher deductibles to decrease your premium, only to be hit by a cost increase on renewal season. Paying a high deductible only to give more money for your bottom line (and give you more headaches) is frustrating, to say the least.

It feels like you’re self-insuring at this point. Don’t worry. You’re not the first to feel this way.

ReNu Insurance Group has worked with over 130 businesses, many of whom were formerly in the traditional market and are now captive owners. They went the route of increasing their deductible, only to be hit with a premium increase on renewal season (and something equivalent to a migraine from the frustration). Their insurance premium almost doubled.

Regardless, going the higher deductible route for a lower premium may not be worth your bottom dollar. Why else would you be here? The point is to relieve the mental agony in your aching brain.

In this article, we’ll lay out why your premiums are increasing on top of your high deductible and other options you can take. That way, you can figure out what insurance option is best for you and no longer feel like you’re self-insuring.

Table of Contents:

- Why is my deductible increasing on top of my insurance premium?

- Are premium costs affected by a line vs class of business?

- Am I better off self-insuring? What are my options?

- Consider captive insurers as an option for your business

Why is my deductible increasing on top of my insurance premium?

When you’re paying higher deductibles, you, the insured, are taking on more risk per claim. You’re taking on more risk while paying the insurer more for your coverage. It seems counter-intuitive, right?

The reason this is happening is because of how the insurer perceives market conditions in:

- The property market

- Workers’ comp

- General Liability

- Auto liability

You might not see it since your business is in a specific geographical location. You may not have dealt with any issues in the past year and have done everything correctly to minimize your risk.

Insurers look at it from a national level, as in all around the United States. Other companies in your industry are causing the insurance company to experience millions or billions in losses. As a result, you’re expected to pay higher premiums to compensate for the carrier’s loss.

Let’s make a hypothetical: You’re an auto dealer in South Carolina and heard about a wildfire that spread across California. It affected auto dealers in that area. Your carrier had to pay for their losses. While you think you’re safe from higher premiums in South Carolina, you see your premium increase on renewal season so your carrier can recover their losses.

Are premium costs affected by a line vs class of business?

Before we get into the answer, let’s distinguish between the line and class of business.

What does line of business mean?

This means the insurance industry is looking at a broader scope of the products or services a business offers. So, the overall nature of a business’s activities.

So think of it as broad categories like construction, retail, manufacturing, finance, etc.

What does class of business mean?

This means what the individual business is actually doing or a more specific categorization. So, think of construction contractors and what each company does independently.

You have more specific categories in construction, like roofing, foundation repair, residential services, commercial services, etc.

Both lines and classes of business will affect your insurance premium cost

Here’s how each can affect your insurance premiums:

- Line of business:

- Risk Evaluation: Insurers assess the overall risk associated with a particular industry or sector. If construction businesses have shown to have higher risks compared to retail, they will likely pay higher premiums. It’s the characteristics of the business that play a role.

- Industry trends within the industry impact your premiums. Insurers adapt pricing based on the landscape and the losses they’re experiencing in the industry.

- Class of business

- The risk factors become more specific. The class of business allows insurers to pinpoint specific risks associated with the activities of the companies—insurers direct premiums based on the specific challenges in the class of business.

- The claims history with a class of business influences premium rates. The higher the claim frequency, the higher the insurer adjusts the premiums for the anticipated risk.

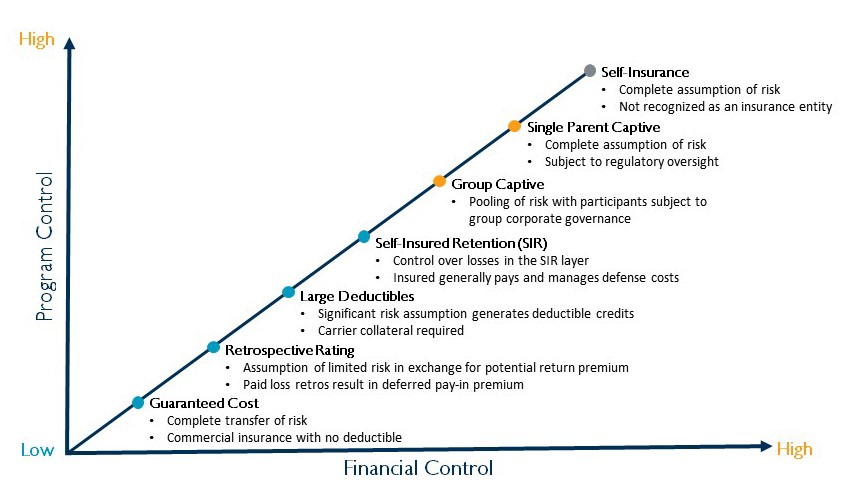

Am I better off self-insuring? What are my options?

If you’re dealing with increased premiums on top of your deductible, it might be time to look for other options. Self-insuring might not be optimal for your business situation, but it’s something to consider. Thankfully, you have plenty of options to consider.

You could find a different carrier that will allow you to pay a larger deductible and lower your premium.

Depending on your line of business, you can do a retro plan, where the carrier sets up a premium based on your loss history. At the end of the year, you figure out if you were over or under on claims. It’s basically like an over-under bet. This option is a little more dangerous. However, plenty of people choose this option.

You can choose to escape the insurance market and become a captive owner. Captives are another option to self-insure and have the backing of a carrier. If you're safety and risk management focused with your business, captives are a strong option for you to consider.

You can be a captive member in a group captive where your pool of risk is with like-minded business participants. Or maybe you can do better with a single-parent captive, where the captive insures only the parent company and its subsidiaries.

Of course, you don’t need to decide just yet. You’ll want to read about the differences between a captive insurance policy vs. a traditional insurance policy.

Look at the graph below to figure out multiple options of what might work best for your business.

Consider captive insurers as an option for your business

ReNu Insurance Group has worked with many captive members who have escaped higher deductibles and premium costs. They are a feasible option. However, you’ll want to see if they’re suitable for your business. Captives aren’t for everyone. They require more robust safety and risk management programs.

The next thing you need to do is read our article on the pros and cons of captive insurance. That way, you can compare the positives and negatives to weigh your insurance options more accurately.

You also need to download and read our free guide, How to Self-Insure Your Business in 90 Days Without Sacrificing the Protection of an Insurance Carrier. It’s a short 30-minute read that provides you with a look at how you’ll get into a captive.

And if you’ve finished this article and said, “I’m not any closer to figuring out another option,” don’t be afraid to schedule a call with ReNu Insurance Group. Because sometimes reading isn’t enough. Talk directly to an expert to help provide you with a better idea of what can work best for you.

Topics:

{kind=link}