Knowing the Financial Benefits of Captive Insurance for Your Business

March 20th, 2024

4 min read

One of the big reasons business owners decide to join a captive is that they’re tired of handing their money to a third-party insurance carrier and want to keep any profit from their risk financing for themselves. After all, the business took on more risk that paid off, so it might as well reap the reward.

Because of strict underwriting guidelines and careful control by the group captive risk committee, group captives tend to be moderately profitable. Insurance companies view profits as “surplus.” Surplus is distributed according to the specific captive’s business plan.

ReNu Insurance Group has given over 130 captive owners insight into how they can make money in a captive—both directly and indirectly—and how to maximize that profit.

After you read this article, you will have a good grasp of this important facet of captive ownership. That way you’ll be able to understand the financial advantages of becoming a captive owner.

You might be wondering how captives can benefit your business. Take this assessment to see how you can profit in a captive.

What are the direct financial benefits of joining the captive?

Captive owners can make money most directly from three sources:

- Underwriting profit/surplus

- Investment Income

- Stabilization of costs

Comparison Table

| Aspect | Traditional Insurance | Captive Insurance |

| Control | Limited, Insurer control policies | Full control over policies and claims |

| Cost Savings | Fixed, often high premiums | Potential for significant long-term savings |

| Risk Management | Insurer manages risk | Customized risk management strategies |

| Investment Income | No direct benefit | Opportunity to earn investment income |

| Profit Sharing | None | Potential for underwriting profit |

| Transparency | Limited insight into cost breakdown | Full financial transparency |

| Tax Advantages | Standard insurance tax treatment | Potential tax benefits |

| Fronting carrier | Not required | Typically required for regulatory compliance |

Underwriting profit

The underwriting profit is what’s left after losses and expenses have been paid out of the insurance premium.

At the end of each year, a traditional third-party insurance company reviews the premiums it has received for that year, assesses its expenses and claims payouts, and keeps what is left as its underwriting profit.

Similarly, if the premium paid into the captive for the year is greater than the loss and expense costs, the captive retains the difference as underwriting profits. This money can be transferred back to the captive as dividends to the group members, or they can be used to help build up the captive's capital and surplus (reserve) funds, which can also earn investment income.

Payout distribution varies by line of business

The payout schedule is super important. Each captive pays out differently. It’s also different by the line of business.

Property claims

- Because there’s very little tail liability on property claims, the majority can be paid out.

- If a policy year ends on December 31, you can see all the claims that would have been submitted in six months.

- With property, you can see whether it got wrecked or it didn’t.

- With certainty, 80% of the underwriting profit, if any, can be paid out. We call it surplus.

- Within another six months after, the rest can be paid out (assuming you haven’t had any other claims).

Claim development causes the liability side to take so long. There’s a correlation between the date the claim is reported and the date of loss. As that gap widens, the claims cost is higher.

So, if a claim is reported three months after the date of loss, you can expect it to be more expensive compared to the one reported within a couple of days of the loss occurrence.

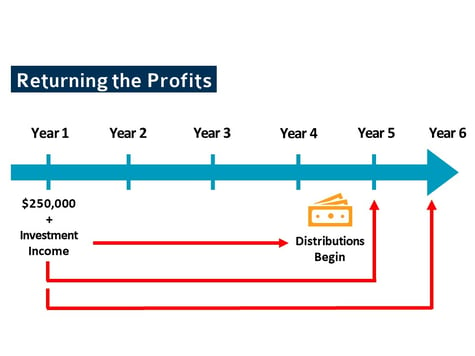

Because of how expensive claims can be, you likely won’t see any of the year one underwriting profit until year four. By the fourth year, depending on the captive structure and what the regulator has approved, you’ll see a percentage of that year one profit. In the years after, you’ll receive more and more of those portions from year one.

You can expect that from other years. If you did well in year two, you can get some of that profit from year five, year three profit in year six, and so on.

You can expect that from other years. If you did well in year two, you can get some of that profit from year five, year three profit in year six, and so on.

It’s only until a policy year’s closed that it’s reconciled, which is decided by a regulator or an actuary alongside a captive manager or a risk committee. Again, it depends on how your captive operates.

Stabilization of costs

With traditional insurance, premiums can change significantly year-over-year based on the underwriting cycle. This is where, if losses are incurred in or across a particular class of business, the insurance market “hardens” in that class. When this happens, all policyholders in the affected class see their premiums raised even if they have had a sterling record for low losses. This fluctuation is made at the whim of the insurance carrier, with no transparency or consultation with the policyholders.

In contrast, captives are not subject to the underwriting cycle. With a captive, the premiums for individual members are based solely on their own loss experience. Renewal premiums can decrease by as much as 28% in the first three years, assuming stable loss experience.

In addition, because the captive members own the captive, they have more negotiating leverage than they could have with a traditional carrier.

What are the indirect sources of profit with a captive?

With a captive, financial gains can be made indirectly through:

- loss reduction;

- loss prevention, and

- ultimate net present value of losses.

Loss reduction

When a business enters a group captive, they share their risk transparently with the other group members, known entities with as much stake as they do and as much to gain. All members' risk management programs are subject to the oversight of the risk management committee, and each member is held accountable for ensuring optimal management of their own risk. This incentive to manage their risk more effectively ultimately leads to loss reduction, which naturally results in a higher balance in the shared profits at the end of the year.

Loss Prevention

Beyond reducing loss, establishing (or strengthening) an effective risk reduction program often includes improving risk control procedures, which can even prevent loss. As above, the result is a larger balance in the shared profit margin for all group members.

Ultimate net present value of losses

Net present value: The discounted value or current cost of an amount to be paid in the future considers anticipated investment income and the timing of tax deductions.

If I’m reserving money today that I won’t need for five years, I’ll earn interest on it until I need it.

What other financial impact would I see if I joined a captive?

As you have seen, there are several direct and indirect ways to make money as a captive owner, whether it's through underwriting profit, investment income, or stabilization of costs.

Other potential financial advantages include cost control, premium deductibility, tax deferral, and estate planning benefits when you're a captive owner.

To learn more about the financial impact of captive ownership, read Will Captive Insurance Help Me With Cash Flow?

And if you are wondering how much you would have to invest to be a captive owner and to see how much underwriting profit you can make, use ReNu Insurance Group's pricing calculator to see your results.

{kind=link}